While the banks’ bad loans have been gradually increasing from the start of the current fiscal year, the NPL deteriorated sharply in the last three months. Bankers attribute the rise in NPL to the slowing economic activities coupled with higher interest rates, and the declining ability of borrowers to repay debts. According to them, loan recovery and debt servicing have become difficult of late.

Banks and financial institutions (BFIs) have started to make their recovery department active after the problems in loan recovery. Many banks have expanded the recovery department by adding additional human resources.

The third quarter of the current fiscal year also saw BFIs slashing their interest rates. In March, the Nepal Bankers’ Association (NBA) fixed the interest rate on fixed deposits for individual depositors at 11 percent. Under huge pressure from the agitated business community, NBA decided to reduce it to 9.99 percent for individual depositors effective from the new year. Similarly, the interest rate for institutional deposits has come down to 7.99 percent from nine percent earlier. Similarly, interest rates on savings account deposits have been set at a minimum of 5.40 percent to a maximum of 7.40 percent.

The commercial banks’ deposits grew by 10.45 percent to Rs 4,764.65bn by mid-April 2023. At the same time, banks’ lending expanded by only 2.66 percent in the first nine months of the current fiscal year.

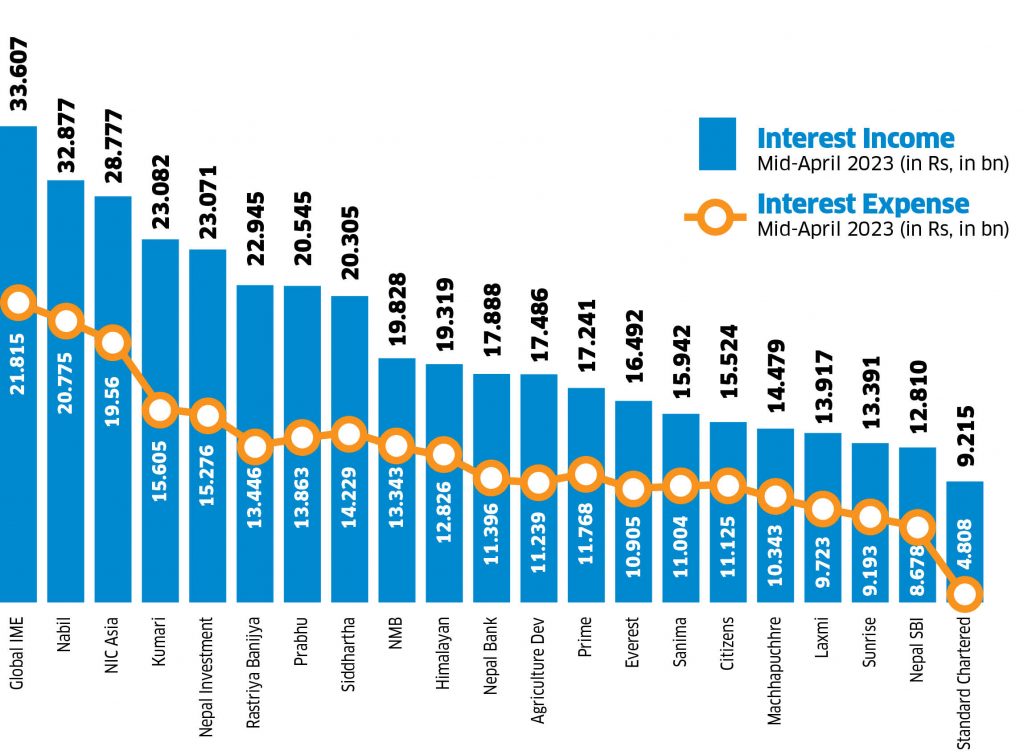

While banks’ interest income grew by 31.60 percent, their interest expenses expanded by much higher during this period. As banks have to pay higher interest rates for deposits amid a prolonged liquidity crunch, their interest expense surged by 34.98 percent. This has affected the bank’s net interest income which grew by 25.43 percent.

Banks saw their net fee income and net trading income shrinking in the first nine months of the current fiscal. The net fee income decreased by 5.03 percent while net trading income shrunk by 36.74 percent during this period.

14 banks’ net profit rise

Despite the problems, the third quarter reports of 21 commercial banks show 14 have increased their profits compared to the same period of the last fiscal year. Similarly, seven banks have reported a decline in profit.

Sunrise Bank, Citizens Bank International, Siddhartha Bank, Prime Commercial Bank, Machhapuchchhre Bank, Agricultural Development Bank, and Nepal Bank have reported a decline in their profits.

The commercial banks’ deposits grew by 10.45 percent to Rs 4,764.65bn by mid-April 2023. At the same time, banks’ lending expanded by only 2.66 percent in the first nine months of the current fiscal year.

While banks’ interest income grew by 31.60 percent, their interest expenses expanded by much higher during this period. As banks have to pay higher interest rates for deposits amid a prolonged liquidity crunch, their interest expense surged by 34.98 percent. This has affected the bank’s net interest income which grew by 25.43 percent.

Banks saw their net fee income and net trading income shrinking in the first nine months of the current fiscal. The net fee income decreased by 5.03 percent while net trading income shrunk by 36.74 percent during this period.

14 banks’ net profit rise

Despite the problems, the third quarter reports of 21 commercial banks show 14 have increased their profits compared to the same period of the last fiscal year. Similarly, seven banks have reported a decline in profit.

Sunrise Bank, Citizens Bank International, Siddhartha Bank, Prime Commercial Bank, Machhapuchchhre Bank, Agricultural Development Bank, and Nepal Bank have reported a decline in their profits.

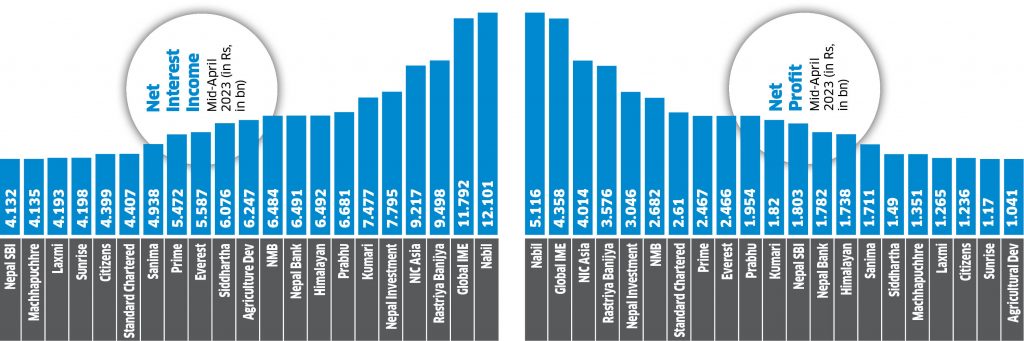

The banks’ quarterly report shows one bank’s profit crossed the Rs 5bn mark, the profits of two banks have crossed Rs 4bn while two earned above Rs 3bn in profit in the current fiscal year.

Nabil Bank records the highest profit

Nabil Bank has topped the chart as the bank’s profit grew by 52.63 percent in the first nine months of the current fiscal year. The bank earned Rs 5.11bn in profit, which is the highest among the banks in the third quarter of the current fiscal year.

Global IME Bank is second on the list with a profit of Rs 4.35bn, an increment of 16.96 percent followed by the NIC Asia Bank which has reported a profit of Rs 4.01bn.

In terms of growth, Everest Bank has the highest profit growth at 62.63 percent. The bank recorded a profit of Rs 2.46bn in the first nine months of this fiscal compared to Rs 1.51bn in the last fiscal. Standard Chartered Bank’s profit also grew by 60.24 percent to Rs 2.61bn.

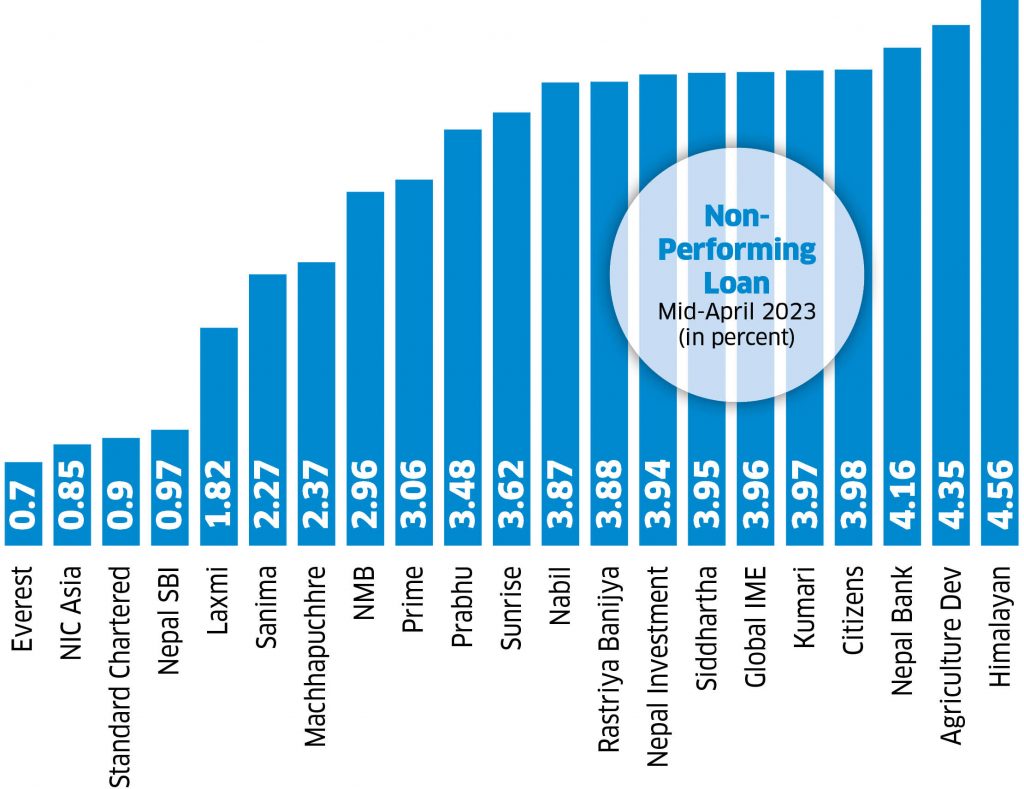

Himalayan Bank posts highest NPL

The profits of banks have also been affected by the increment in bad loans as they have to keep aside large amounts of money for the provisioning of bad loans. Provisioning is a practice where banks are required to maintain a certain amount in reserve when loans are not recovered.

Among the commercial banks, the NPLs of three banks crossed four percent. Himalayan Bank has the highest NPL of 4.56 percent, followed by the Agricultural Development Bank with 4.35 percent, and Nepal Bank with 4.16 percent.

Four banks have managed to keep their NPL below one percent. Nepal SBI Bank, Standard Chartered Bank Nepal, NIC Asia Bank, and Everest Bank have less than 1 percent NPL. SBI’s NPL stood at 0.97 percent, Standard Chartered’s at 0.90 percent, NIC Asia’s at 0.85 percent, and Everest’s at 0.70 percent.

Provisioning surged by 324.27 percent

As NPLs surged sharply, the loan loss provisions of banks also increased. The amount for provisioning has increased by 324.27 percent. Banks have set aside Rs 31.32bn for loan loss provisions till mid-April 2023 compared to Rs 7.38bn during the same period of the last fiscal year. The total provisioning amount of banks increased by Rs 23.94bn in the last 12 months.

Kumari Bank and Nabil Bank have set aside above Rs 3bn each for provisioning purposes in the third quarter.

The banks’ quarterly report shows one bank’s profit crossed the Rs 5bn mark, the profits of two banks have crossed Rs 4bn while two earned above Rs 3bn in profit in the current fiscal year.

Nabil Bank records the highest profit

Nabil Bank has topped the chart as the bank’s profit grew by 52.63 percent in the first nine months of the current fiscal year. The bank earned Rs 5.11bn in profit, which is the highest among the banks in the third quarter of the current fiscal year.

Global IME Bank is second on the list with a profit of Rs 4.35bn, an increment of 16.96 percent followed by the NIC Asia Bank which has reported a profit of Rs 4.01bn.

In terms of growth, Everest Bank has the highest profit growth at 62.63 percent. The bank recorded a profit of Rs 2.46bn in the first nine months of this fiscal compared to Rs 1.51bn in the last fiscal. Standard Chartered Bank’s profit also grew by 60.24 percent to Rs 2.61bn.

Himalayan Bank posts highest NPL

The profits of banks have also been affected by the increment in bad loans as they have to keep aside large amounts of money for the provisioning of bad loans. Provisioning is a practice where banks are required to maintain a certain amount in reserve when loans are not recovered.

Among the commercial banks, the NPLs of three banks crossed four percent. Himalayan Bank has the highest NPL of 4.56 percent, followed by the Agricultural Development Bank with 4.35 percent, and Nepal Bank with 4.16 percent.

Four banks have managed to keep their NPL below one percent. Nepal SBI Bank, Standard Chartered Bank Nepal, NIC Asia Bank, and Everest Bank have less than 1 percent NPL. SBI’s NPL stood at 0.97 percent, Standard Chartered’s at 0.90 percent, NIC Asia’s at 0.85 percent, and Everest’s at 0.70 percent.

Provisioning surged by 324.27 percent

As NPLs surged sharply, the loan loss provisions of banks also increased. The amount for provisioning has increased by 324.27 percent. Banks have set aside Rs 31.32bn for loan loss provisions till mid-April 2023 compared to Rs 7.38bn during the same period of the last fiscal year. The total provisioning amount of banks increased by Rs 23.94bn in the last 12 months.

Kumari Bank and Nabil Bank have set aside above Rs 3bn each for provisioning purposes in the third quarter.